Vertiv’s (NYSE: VRT) Q1:2026 sales increased 30%, organic sales increased 23%, and adjusted operating margins expanded 430 basis points year-over-year. The operating margin expansion was driven by operating leverage (high sales volume on their fixed manufacturing base), Vertiv Operating System (VOS) efficiencies, and pricing power. This led to adjusted EPS growth of 83%.

Free cash flow (FCF) increased 147%, driven by surging profits and efficient management of working capital (remember that the balance sheet can be a source of cash). Vertiv generated an FCF margin of about 25% and FCF conversion on adjusted net income of over 140%. The 147% year-over-year growth in FCF was especially impressive considering Vertiv increased CapEx by 208% to increase capacity to meet growing demand.

Following the strong start to the year, Vertiv raised full-year 2026 guidance, now expecting revenue of $13.5 billion to $14 billion (up from $13.25 billion to $13.75 billion) and adjusted EPS of $6.30 to $6.40 (up from $5.97 to $6.07). Vertiv’s guidance for 2026 implies sales growth of 34% and adjusted EPS growth of 51% at the mid-point.

Key takeaways from the call…

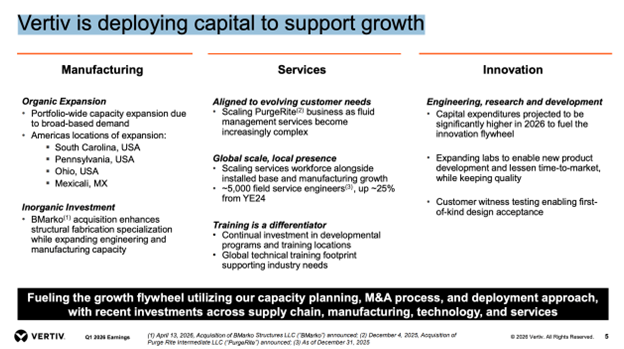

(1) Vertiv is aggressively working to increase capacity (by increasing CapEx as a % of revenue, making acquisitions, and increasing the number of field service engineers by 25% to 5,000 since year-end 2024) to support surging demand for data center thermal and power equipment and services. You can read more about recent capacity expansion actions here, here, and here.

(2) Regarding M&A specifically, Vertiv CEO Gio Albertazzi stressed that the balance sheet is very strong with net debt-to-EBITDA of only 0.2x and that the acquisition pipeline is “very active.” He also said that Vertiv would not hesitate to do larger deals when the opportunity presents itself. Specifically, he said Vertiv would “have no reticence in cutting bigger checks” and that the company has “no fixed limits” regarding acquisition size. In fact, five days after the earnings call (on April 27th), Vertiv announced yet another liquid-cooling acquisition.

(3) The most important takeaway is that Vertiv is experiencing increased demand for pre-fabricated (modular) solutions that integrate thermal and power into one system. In other words, the data center builders/owners are shifting from buying discrete parts from different vendors to integrated systems from the leading vendors that can provide customized (co-designed), turnkey solutions across technologies that are required to work in unison (like cooling and power).

I think the vendors that will benefit most in this environment are the ones with: the largest R&D budgets and long-term co-design relationships (meaning they have a seat at the table and are working on rack-level and broader data center designs two or three generations into the future), the manufacturing capacity to meet customer demand (speed-to-token), the balance sheets and cash flow to fill in puzzle pieces with acquisitions, and 24/7 global service teams to keep everything running as efficiently as possible (efficiently means max uptime while using and losing as little energy as possible to drive revenue in a cost-effective manner).

These pre-fabricated, converged systems provide faster build/deployment times (so faster time-to-token) and better efficiency because of the way that thermal and power equipment is optimized in a single system solution. The rapidly increasing technological complexity, customization, and converged nature of data center systems increases the franchise value of having the best global service team in the industry (said another way, it decreases the likelihood that data center operators will outsource service to a third-party). The shift to integrated systems is a topic I discussed on the Rebellious Allocations podcast episodes for both Vertiv and Eaton.

(And btw, as mentioned in several of my notes, business models based on a large and growing installed base of hardware (that is often infused with proprietary software) with a higher-margin services business attached is a common quality you will find across the Bastion Industrial and Infrastructure portfolio. As the installed base grows, so does the annuity stream of higher-margin monitor, maintenance, repair, and replace revenue. Holdings in the portfolio that share this pattern include Vertiv, Trane, KLA Corporation, Eaton, GE Vernova, and GE Aerospace).

(4) Vertiv is holding an investor day on May 19th-May 20th, where they plan to give an “updated multiyear outlook.” I think that means they plan to raise long-term financial targets.

The world feels more uncertain than ever, but I sleep well at night partnering with Dave Cote and Gio and letting them navigate some of that uncertainty on our behalf.

Key quotes from the earnings call…

(note: bold and underline are my own)

“What we’re seeing in customer conversations is different than 6 months ago. The urgency has increased. The scale of deployments is larger and the technical complexity is creating opportunities for companies that can solve system-level problems, which is exactly where we excel. We’re seeing broad-based strength, and that tells you something about the depth of demand and our ability to capture it. I like what we’re seeing in the industry and the continued evolution of Vertiv. We’re still in the early stages of the infrastructure build-out for AI. Our competitive advantages are compounding. If you can deliver products, systems, integrated solutions and services at scale, you become even more important to your customers’ technology road maps…We’re expecting a strong year ahead and strong years in the future.”

“We are accelerating our strategic capacity investments to meet the demand we are seeing. We’re expanding our global manufacturing service footprint while unlocking latent capacity with VOS-driven productivity gains.”

“We continue to see very robust growth in demand for data centers. And as a result, we are focusing investments on capacity expansion, supply chain and engineering capabilities. We are committed to continue to grow capacity supporting our customer demand, and we continue to deliver above-market growth. Our CapEx in Q1, sustainably higher than in the same quarter last year is testament to that commitment. We are making significant investments in capacity expansion across both manufacturing and services.”

“On the manufacturing side, we’re expanding capacity organically across multiple sites globally and particularly across the Americas, of which you see some details here. These investments are strategic and position us to meet the accelerating demand. We do this for growth, but also to bolster our overall operational resiliency. This capacity expansion is broad-based, power management, thermal management, infrastructure solutions and IT systems across all technologies. We’re doing the same with our services capability. Specifically, we are scaling our people and service capacity vigorously and convincingly across all service technologies and regions. In particular, the acquisition of PurgeRite significantly strengthens our fluid management and liquid cooling capabilities, enhancing our system-level services offering. This is one of the most technically demanding and financially consequential aspects of modern data center operations.”

“Our long-standing customer relationships, combined with our deep partnerships create a significant competitive advantage that is very difficult to replicate. We continue to move further and the market is recognizing it. Achieving investment-grade credit ratings and inclusion in the S&P 500 are meaningful milestones. They reflect the strength of this business, the execution prowess of this team and the confidence the market has placed in our trajectory. I do not take that lightly, neither does the rest of the Vertiv team. We hold ourselves to a high standard and will continue to raise the bar. We had a strong quarter. We expect to build on it, and we will.”

“One is we know that speed or time to token is absolutely essential in the market. Clearly, prefabrication alleviates challenges on site, a construction site is always a complex system to manage. There is a scarcity of talent, trade resources. We see and we certainly are stimulating, if you will, an increasing adoption of prefabrication. But there is way more to it than that. For us, prefabrication is not just prefabrication. It’s convergence of our solution into a system like OneCore, not only OneCore, but OneCore, SmartRun, et cetera, system that are designed, converged and optimized already from the beginning on a given set of louvers and silicon. And it is also a way to make the whole system more efficient and more dense in many respects. So there are multiple reasons why this is being adopted. And there are multiple reasons why we believe we are ahead of the pack here because we are not just an integrator.”

“We’re constantly adding capacity. But as you could see from our CapEx profile and what we mentioned about Q1, we’re very, very focused on adding capacity and a lot of that capacity starts to hit us in the second half.”

“What we like when we talk in general about services is the fact that the installed base that is being created is very, very conducive to our life cycle capture and business over time.”

“So overall incremental margins were always in the neighborhood of 30% to 35%. I would say that would kind of be similar in terms of the way that we would expect services to pull through as well.”

“That’s why we were talking about a coiled spring because there is a shortage of data center capacity, significant shortage of data center capacity and even more profound shortage of AI capable data centers in EMEA and in Europe, in particular. So hence, the dynamics that you see. And of course, we are very well positioned in Europe because of historically a strong presence, but also because a lot of the players are players here and are players in Europe. So there is a very encouraging opportunity there.”

“I think we go back to what we’ve said all along is there’s 2 spaces where we love to invest in on a regular basis, and that’s the ER&D book and the capacity book. And you can see on the flow-through of our cash statement that we’re following with that drumbeat. That’s what we like to do, and that’s where you see us continue to invest heavily. The other portions of that are capital deployment in terms of M&A or stock buyback or increased dividends. I think the biggest area that we had to use cash there and that we always look to have some dry powder would be the M&A space. We’ve done some this quarter, as you saw. I think we’d continue to keep that open and that optionality available for us.”

“M&A pipeline is very active. You have seen us do acquisitions that are bolt-on predominantly technology-based. We love technology. And our pipeline is well structured and quite convincing. So we’ll continue to be focused on this area of capital deployment, too.”

“But if we go to supercompute, the center stage was our SmartRun solution, which is the entire white space infrastructure comprising everything, white space data hall, power distribution, liquid cooling. So I would say that the integration and the convergence of that solution across multiple technology areas that normally happens on site with great consumption of time and cost is something that we have changed dramatically with the SmartRun. So SmartRun is extremely successful. And I think we have done our part again to change the way the industry works.”

“Well, certainly, convergence [of technology across power and thermal] is very important. And as I was saying, it’s not just prefabrication, but it’s an optimized system. That’s why having an optimized system with Vertiv technology is a winner. But we shouldn’t think about this as replacing the point-to-point, let’s say, the product point type of activity. It is a gradual and partial shift. And really different players have different degrees of adoption. So if you think about power modules, those are pretty much becoming a standard in the industry. So you’ll see that people will start to buy power modules instead of necessarily going into each and every component inside. It’s never black and white, but that’s a direction. When it comes to the entire converged system, the entire manufactured system, SmartRun, well, the interfaces might be slightly different. But again, it’s not a totally different breed of players or people you discuss the engineering or the transaction. But there is also a different category of people in the industry that might not have historically that type of procurement or engineering staff and experience nor do they need it when someone is capable of providing an already fully optimized pre-engineered converged system and solution. So the market is taking multiple — going in multiple directions. Some are partially overlapping, some are different. So we are very happy about our point product and-to-point product, let’s say, type of business as well as we see integration and convergence becoming a bigger part of the market that we serve.”

“So we have no reticence in cutting bigger checks when that’s needed and what’s opportune, let’s say, as we have demonstrated. And our balance sheet is certainly very, very strong. And when we see value, we go for value. And value is not just per se, there’s value in the context of our long-term strategy and our technology and market growth strategy. So rest assured that we have no — how can I say, no fixed limits in that perspective.”

Key slides (blue highlights my own…

Disclosure: John Rotonti is an investor in and the portfolio manager of the Bastion Industrials and Infrastructure Portfolio, which owns shares of Vertiv, Trane, KLA Corporation, Eaton, GE Vernova, and GE Aerospace.

Disclaimer: This article is intended for informational purposes only and does not constitute tax, financial, or legal advice. Investing carries risks, including potential loss of principal. Consult a qualified professional for personalized recommendations and to ensure compliance with applicable tax laws and regulations.