Trane’s (NYSE: TT) full-year 2025 revenue increased 7%, organic revenue increased 6%, adjusted operating margins expanded 90 basis points, and adjusted EPS grew 16% to $13.06. It generated a return on equity (ROE) of 34%, which is in-line with 2024 levels.

Free cash flow (FCF) increased 3.5% to nearly $2.9 billion, resulting in an FCF margin of 13.5% and FCF conversion on adjusted net income of 98%. Trane returned over $2.3 billion to shareholders as dividends and buybacks in 2025 compared to about $2 billion in 2024. In 2025 Trane increased the dividend by 12% (dividend up 77% since March 2020) and it has $4.7 billion remaining on its repurchase authorization (equal to roughly 5% of the market cap).

These results are solid considering two of its end markets, residential and transportation (refrigerated trucking units), are in recessions. For 2026, Trane is guiding for organic revenue growth of 6% to 7%, total revenue growth of 8.5% to 9.5%, incremental operating margins of at least 25%, FCF conversion of at least 100%, and for adjusted EPS of $14.65 to $14.85 (implying growth of about 12% to 14%).

Importantly, Trane is expecting its residential market and transportation market to “trough” in the first half of 2026. Trane expects residential demand to improve in the back half of 2026 and for its transportation market to improve late in 2026 or into 2027.

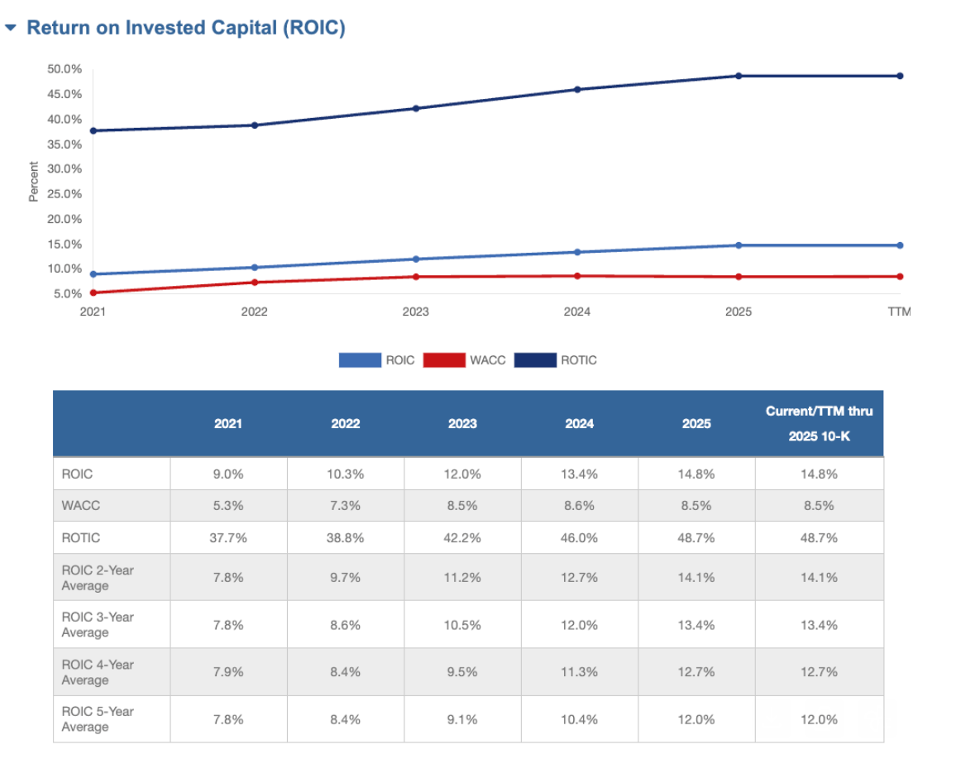

Since the spin-off from Ingersoll Rand in 2020 through year-end 2025, Trane’s revenue increased at an 11% compounded annual growth rate (CAGR), EBITDA margins expanded 470 basis points, it generated FCF conversion of 106%, and adjusted EPS compounded at 24%. According to New Constructs, Trane’s return on invested capital (ROIC) and return on tangible invested capital (ROTIC) increased in each of the past four years with its ROTIC approaching 50%.

The most important takeaway to me from the call is that Trane expects that its two drags on earnings growth (residential HVAC and refrigerated trailer units) are close to bottoming. Additionally, in Q4:2025 Trane generated “broad based growth” in 12 of the 14 verticals it sells commercial HVAC units into (note: AI data centers is only one of the 14 commercial verticals). This commentary from Trane, along with some other industrial data points I’m tracking, corroborates the early recovery in broad industrial end markets discussed by Amphenol and TE Connectivity on their December-quarter earnings calls. I still have lots of earnings transcripts to go through to build higher conviction that the U.S. may be coming out of its industrial and housing recessions, but I’m hopeful and will continue to monitor.

Now for a long discussion on the future of chillers in AI data centers…

At CES 2026, Nvidia CEO Jensen Huang said that with the new Vera Rubin GPU server racks “no water chillers are necessary for data centers” because the racks can be fully chilled with liquid cooling technologies like those offered from Vertiv or Boyd (being acquired by Eaton). This obviously sent HVAC investors into a tizzy. A lot of the call was focused on the future of chillers in the data center, and I encourage you to read the bold and underlined quotes below to get a fuller picture. But Trane CEO Dave Regnery said that, “when we’re sitting with these customers [planning reference design AI factories two to four years into the future]…I have not seen a reference design or data center of the future that does not include chillers, just to be very clear.” Regnery continued that, “we’ve been very strong in the data center vertical for decades, and we’re going to continue to be very, very strong well into the future.”

And Regnery’s words are supported by a joint Trane-Nvidia press release dated October 28, 2025 saying that Trane launched the “industry’s first comprehensive thermal management system reference design, specifically engineered” for Nvidia gigawatt-scale AI factories. The press release even highlights the system is designed for Nvidia’s latest-gen GPU rack architectures including Rubin, saying the design “supports the advanced power and cooling needs of NVIDIA GB300 NVL72 infrastructure, ensuring optimal performance for Blackwell and next-generation NVIDIA Vera Rubin systems.”

So, given Trane’s close partnership with Nvidia and a reference designed specifically to work with AI factories stacked with Rubin GPU racks, the fact that chillers will very likely still be needed to extract hot air out of the building, and Trane’s investment into its own liquid cooling solutions, I’m just not worried at this point.

Now, if you’re looking for some bearish red meat, Regnery did speculate that chillers might not need to run as often in future AI factories, which could mean less wear and tear on the mechanical systems, and therefore a lower level or shorter tail of higher-margin services revenue attached to the installed base. Regnery explains, “Hey, if a chiller runs less, do you have the same service on it?” And the reality of it is in a data center, think of it as a chiller — the fan side or the air side of the chiller is going to run as it does today. The compressing side of the chiller may run less, but it still has to run. And if you don’t run it, you’re going to end up with problems [just like if you don’t run your car because it’s a mechanical system].”

But, on the positive side, these applied systems designed for data centers are so complex that it almost guarantees that Trane gets the service contract over a third-party service provider. On the call, Regnery said, “if you go back, like, say, a decade ago, I don’t think our attachment rate [the rate at which a service contract is attached to a unit sale] was nearly what it is today. In fact, I’d be hard-pressed to think where we’ve done a major chiller farm where we haven’t had the service agreement.”

Once again, I’m just not worried yet. Trane is an extremely well-managed, innovative, adaptable business. It is a multi-industrial with a residential business, a transportation business, and a large and fast-growing commercial business that sells into 14 verticals (with AI only being one of them).

And that commercial vertical (and specifically the AI data center portion of it) is growing like gangbusters. Trane has record backlog, which is being driven by its Americas commercial HVAC business. Its applied business inside of commercial HVAC (bespoke, highly customized solutions like the one designed for Nvidia above) had bookings growth of 120% in Q4:2025 with a record book-to-bill of 200%. This was the second consecutive quarter with applied solutions booking growth over 100%. Despite all the concerns over waning demand in AI, growth seems to be accelerating.

This “exceptional bookings growth” and record backlog not only strengthens Trane’s “visibility into strong growth in 2026 and beyond”, but gives me confidence that its AI business is doing great and will continue to do so. Regnery said, “Even after 2 consecutive quarters of more than 100% applied growth in Americas commercial HVAC, we continue to see substantial opportunities ahead.”

Oh, and Trane acquired Stellar Energy, a leading provider of turnkey data center cooling solutions using modular designs. The modular designs allow Trane to assemble complex chiller systems on site at a data center like LEGOs, saving time and labor (there is a massive shortage of skilled mechanical laborers in the U.S.).

Trane is IMO one of the highest quality industrial technology companies in the world, and it’s getting better. I think it has a wide and durable moat based on its brand, global scale and distribution (with 7,500 service techs around the world), highly trained direct commercial sales force with deep industry connections, and the industry leading software simulation platform used for HVAC system design and monitoring (btw even if those data center chillers do run less, they are still going to have the software services monitoring attached).

Trane has historically increased prices annually, and also has the ability to increase prices further during periods of higher inflation (ex: it increased prices 10% in 2022 and an additional 5% in 2023 to offset input cost inflation). Trane’s business model is very “capex-light” and typically generates 25%+ incremental operating margins, which supports modest margin growth each year (20 or 30 basis points at least), rising returns on invested capital, and strong FCF generation.

I think that Dave Regnery is an exceptional CEO with a growth mindset. He “reinvests relentlessly” into innovation but minimizes CapEx by utilizing lean manufacturing and M&A (Trane has made over 25 acquisitions in the last 5 years), which are sometimes more capital-efficient ways to add manufacturing capacity than CapEx. He sets guidance that he thinks the company can “meet or exceed” and he’s committed to returning 100% of FCF to investors over time.

Additionally, Trane is positioned to profitably grow from the long-duration secular growth tailwinds of energy efficiency, onshoring/near-shoring of manufacturing, and decarbonization.

Regarding decarbonization, Goldman Sachs Sustain put out a report dated Oct 10, 2025 saying that energy efficiency gains across the world have played a greater role in avoiding carbon emissions than deploying renewable energy generation (energy efficiency gains contributed 60% and renewables 40% to avoided emissions from 2010 to 2022). Trane has set the “Gigaton Challenge” where it has set a goal to reduce one billion metric tons of its customer’s greenhouse gas emissions by 2030. One billion metric tons is equal to 2% of the world’s annual emissions (which is equal to the yearly emissions of the U.K., France, and Italy combined). Trane is positioned to do this because heating and cooling buildings accounts for about 15% of the world’s carbon emissions (according to the world economic forum). Trane plans to accomplish this goal by designing machines that are more energy efficient (use less electricity), replacing gas-powered boilers with electric heat pumps, using sensors and AI to monitor machine leaks (refrigerants are a greenhouse gas), and designing machines that use next-gen lower GWP (global warming potential) refrigerants.

(By the way, a related way to make buildings more efficient is with insulation because well insulated buildings can stay warmer in the winter and cooler in the summer, thereby reducing the reliance on HVAC. And we have two companies with exposure to insulation, Carlisle Companies which manufactures it, and Installed Building Products, which primarily installs it).

One of the topics I discuss with my clients a lot is investing in companies with clear value propositions, and Trane is a perfect example. Its heavy commercial (applied) systems help its customers reduce carbon emissions and energy use so the payback (return on investment) to the client is fast (measured in only a few years). To be clear, this isn’t about virtue signaling ESG. Rather, this is about one company that has the installed base, technology/engineering prowess, and future demand that can have a real, measurable, and positive impact on the planet.

90% of Trane’s backlog falls within its commercial HVAC segment (CHVAC), which sells highly complicated and customized/bespoke applied HVAC units into mega projects such as data centers, semiconductor foundries, medical facilities, universities, and skyscrapers. Yes, its data center business has been growing like a weed, but data centers are only one of 14 commercial verticals that it sells into. So, its commercial business is diversified by vertical and geography. Additionally, and important to the investment thesis, it has a large and growing installed base (with over 65,000 connected/monitored buildings and over a million pieces of connected equipment) and these applied units are so complicated and customized that they provide a roughly 25-30-year lifetime of higher-margin service revenue that Trane estimates is equal to 8x – 10x the initial price of the machine. This service revenue is higher-margin, predictable, and most of it is still in front of the company (has not been recognized yet). Currently, service revenue makes up about a third of total sales and is growing at a low teens rate. I believe the services business will provide Trane with durable growth and further transform the company into an even higher-margin, higher-ROIC business over the next 10-20 years. In other words, I think we are still in the early stages of a long-duration profit cycle at Trane that should drive a long runway of 10%-15% annualized per-share growth.

Sources: official materials and webcast

Disclosure: John Rotonti is an investor in and the portfolio manager of the Bastion Industrials and Infrastructure portfolio, which owns shares of Trane Technologies, Nvidia, Amphenol, TE Connectivity, Vertiv, Eaton, Carlisle Companies, and Installed Building Products.

Subscribe to JRo’s Notes newsletter to see select presentation slides and call notes that John highlights.

Disclaimer: This article is intended for informational purposes only and does not constitute tax, financial, or legal advice. Investing carries risks, including potential loss of principal. Consult a qualified professional for personalized recommendations and to ensure compliance with applicable tax laws and regulations.