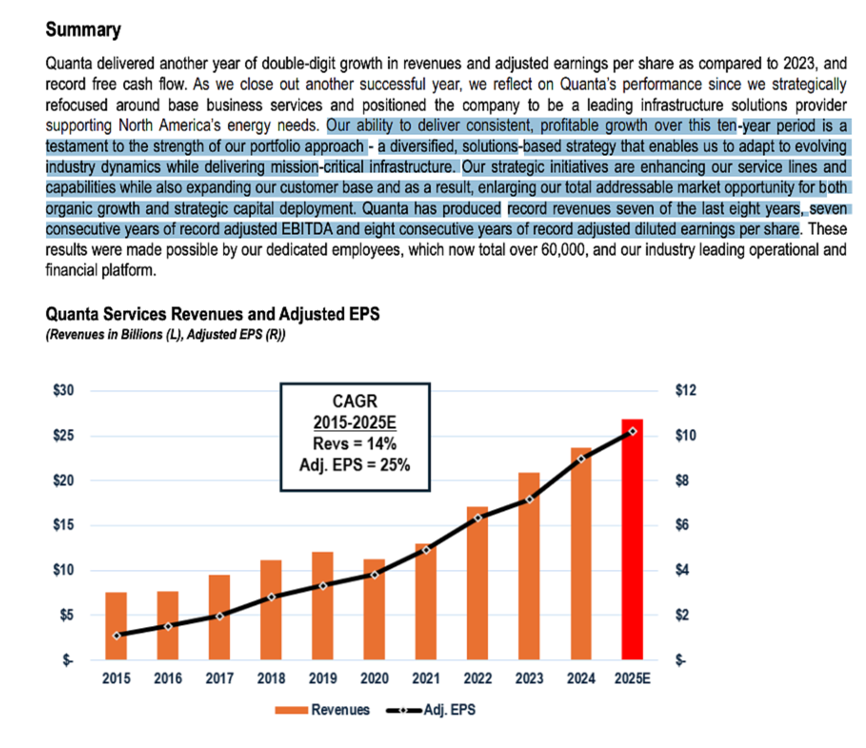

Quanta’s (NYSE: PWR) business is performing very well. Its Q1:2025 revenue increased nearly 24% and its adjusted EPS grew 26% from the same period in the prior year. Its backlog grew to $35.3 billion. The impressive thing about Quanta’s EPS growth is that it has been able to sustain this level of growth for a decade (see first screenshot below from its Q4:2024 management commentary). Not bad for an “electrical contractor” (more on this in a moment).

Following the strong start to the year, Quanta raised the mid-point of its full-year 2025 guidance for revenue and adjusted EPS. It now expects full-year revenue of $26.7 to $27.2 billion and adjusted EPS of $10.05 to $10.65 (up from of $9.90 to $10.50). Quanta also received a credit rating upgrade from S&P in the quarter.

Quanta generated about $118 million in free cash flow (FCF) in the quarter, which is down about 35% year-over-year. But that is because of a $109 million tax payment (deferred from 2024) so that’s a cash outflow, and because CapEx increased nearly 60%. Quanta’s management team is still expects to generate $1.2 billion to $1.7 billion in full-year 2025 FCF. Quanta is focused on improving its FCF over time by driving growth but also through tighter working capital management and improving its cash conversion cycle (collecting payment quicker from clients). Quanta’s days sales outstanding (DSOs) were 63 in the quarter, which is down from 71 in the same period last year and down from a 20-quarter average of 77. This management team clearly understands that its balance sheet can be a source of cash flow, and I expect that Quanta will be generating over $2 billion in annual FCF within a few years (and maybe sooner).

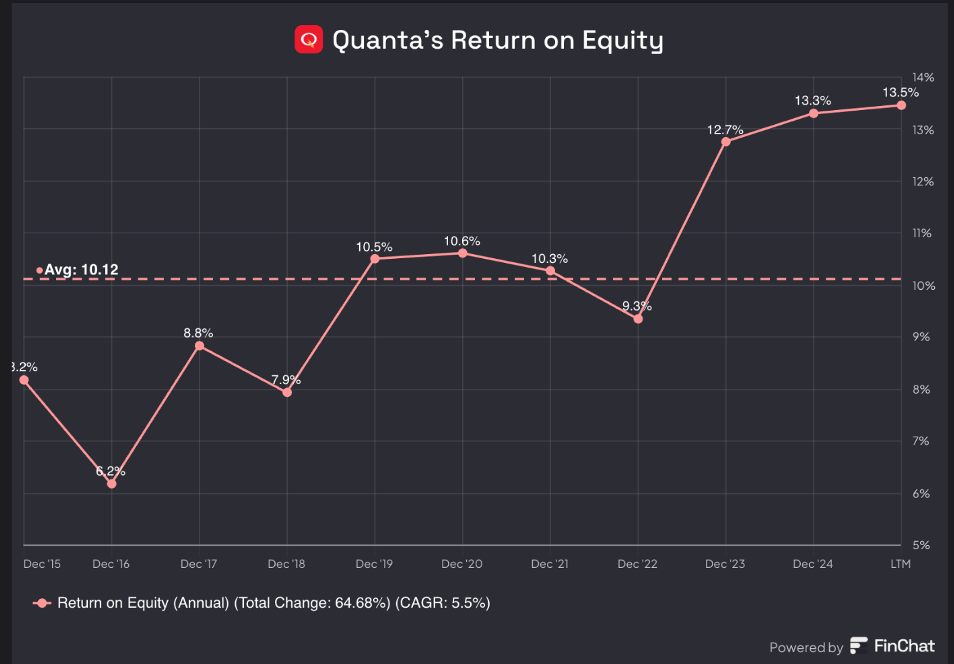

Quanta generated a return on equity (ROE) of 13.5%, which is above its five-year (2020 – 2024) average ROE of 11% and above its 2015 to 2018 average ROE of less than 8%. This is a step-function shift in Quanta’s return-profile in the last decade. In the second image below, you can see that in the last decade Quanta has had three distinct phases of returns…the first when ROEs were around 7%-8%, then a middle phase when ROE was around 10%, and now this latest phase shift with its ROE above 13%, and rising.

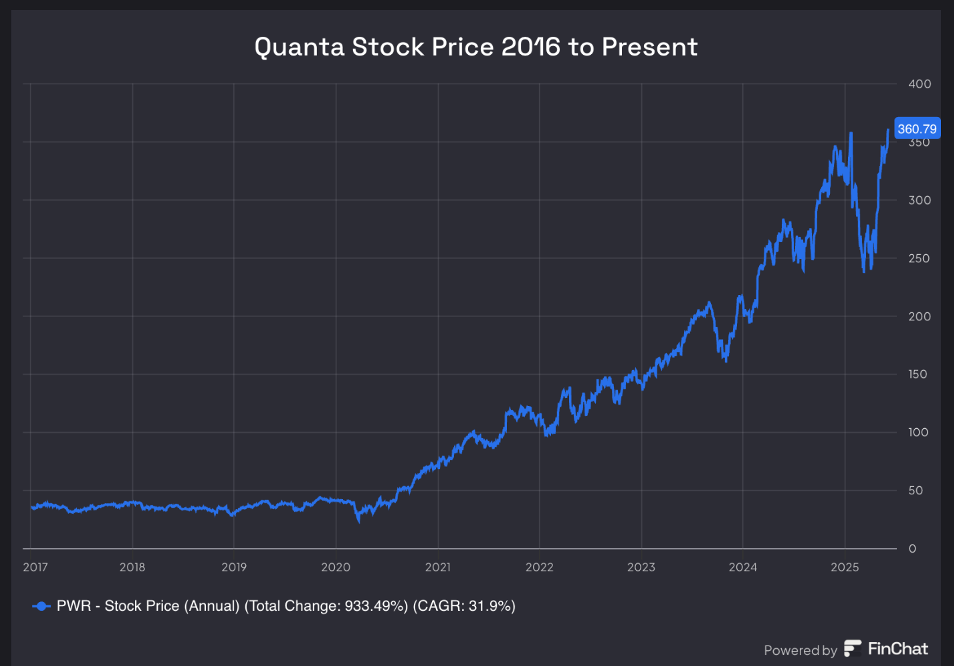

The combination of its sustained high EPS growth plus rising returns led to P/E multiple expansion (third image below) because a company with sustainably high per-share growth and rising returns deserves to trade at a higher valuation multiple. And the combination of annualized EPS growth of 25% plus the additional tailwind from the re-rating (higher) of the P/E multiple drove around 30% annualized growth in the stock price (fourth image below). For those that identified Duke Austin as a transformational and generational leader early on, well done.

One of the reasons that Quanta has been able to sustain such high growth is because it’s the best operator with the most available (and best trained) labor capacity in big, important markets with accelerating growth.

But I think an equally important reason why it’s been able to grow per share value at a mid-20% annualized rate while expanding ROE is because Earl “Duke” Austin was appointed CEO in 2016 and since then he has completely transitioned the company from being an electrical contractor (commoditized type of work with lower ROE) to a turnkey electrical grid, renewables, and technology infrastructure solutions provider. As a solutions provider Quanta handles all the project’s permitting, planning, design, engineering, construction, and even procurement and in-house manufacturing of transformers here in the U.S. This one-stop-shop solution adds more value to the client, creates client stickiness, and allows Quanta to grab higher wallet share so carries higher margins and returns.

Duke also used acquisitions to expand the total addressable market (TAM), which further drove growth, margins, and returns. In other words, Duke architected a better business model and led efforts to build a moat around that business. This is not easy work, but Duke is a builder, and he did it, and I don’t think he’s even close to done. My analysis leads me to believe the moat is durable and growing wider at a time when Quanta’s services are as crucial as ever.

To justify its NTM P/E of 33x I think Quanta need to find ways to maintain an EPS growth rate of at least mid-teens while expanding returns on equity further. I expect this to happen, and Duke Austin recently suggested that the company’s pipeline of work is long and that he thinks the company’s returns can grow faster than margins and possibly even grow at rates in line with organic growth. This is very encouraging news for long-term investors.

The following quotes come from Quanta’s first quarter earnings call transcript, the Q1:2025 management commentary document, as well as from the recent Bernstein Strategic Decisions Conference (SDC) on May 28th, 2025, suggesting that Quanta’s management is very bullish on the long-term opportunity for growth, improved earnings visibility/predictability, and improved margins and return on invested capital (ROIC)…

“We believe we are in the early stages of this infrastructure cycle and that Quanta’s capabilities across generation, delivery and consumption of electricity make us well positioned to deliver solutions to these large and growing addressable markets.

“The growth opportunities across our end markets are extensive, and we believe the drivers of demand for our infrastructure solutions are long-term in duration and create opportunity for multi-year earnings visibility.”

“Even with regulatory and macroeconomic dynamics creating uncertainty in areas of the market, our first quarter performance and the momentum across our portfolio of solutions gives us increased confidence for the full year 2025 and we believe there is a path toward the high end of our updated financial expectations range.”

“We believe electrification and increased load growth will require significant capital investment, and we believe Quanta is in the early stages of a multi-decade infrastructure build. The convergence of the utility, power generation and technology industries is gaining pace and our strategic acquisitions, including Cupertino Electric, enhances Quanta’s presence at the nexus of this convergence. We believe the strength of our end markets, our execution capabilities and our proven ability to strategically deploy capital will allow us to continue delivering improved returns and generate significant long-term stockholder value.”

“The energy and infrastructure landscape is undergoing a fundamental transformation, and Quanta is positioned at its center. Utilities across the United States are experiencing and forecasting meaningful increases in power demand, which is being driven by the adoption of new technologies and related infrastructure, including data centers and artificial intelligence, policies intended to reinforce domestic manufacturing and supply chain resources and the need for all forms of energy generation. We believe these drivers are leading to what could become the largest investment and an expansion of high-voltage transmission infrastructure in a generation.”

“I don’t think there’s any shortage of projects on the wall, I’ll say that. If they all go, then we’ve got a lot of work for the next two decades. So — but I think we got it either way.”

“We are seeing more material pull-through as well [so] at the same margins, return on invested capital is going to come through higher. So, I think the returns go up as well in this market.”

“And so those are the places I would point to where you can see large transmission getting built. We’re in early stages of it. At the very early stages. And I do think you’ll continue to see us stack work over the next five years.”

“We sit at the nucleus of what I consider one of the biggest builds of infrastructure that we’ve seen.”

“I think the grid could really double generation for sure and what we see going out, call it, 20 years or so, I think, somewhere in there. But in general, I see a great demand. Some of it is data center driven, some of it’s onshoring, some of it is just growth. I mean we had appliances, and we made a lot of headway there. We do have battery vehicles, probably, I would say that slowed, it’s lower than kind of how I thought about it. But I would say data centers and everything else has exceeded that demand. And I think we can see out a decade or more of really kind of good build growth. I know sometimes these articles and big jobs, monuments, I’ll call them, they take the headlines. But underneath is just solid growth and just a very, very paced infrastructure build. You can look at our capital on utility capital or you can look at technology capital and see that growth come and then we can’t meet demand today. I mean if you look at turbines, they’re out, I don’t know, 5 years, I guess, is the average, someone else would know better than me. But at least, call it 5 years in turbines. And so when you look at gas being out that long, you have to come in with the renewables and things that you can — batteries, things that you can do today. And so that’s — really the angst is to go faster in AI, push the data centers, push onshoring. You can’t do that without generation and transmission. So I continue to believe you’ll see significant amounts of transmission build as well as generation behind it, lots of renewables, probably solar batteries for the time being, some wind, and you’ll get some gas generation built in here for really what I consider to probably double the load of the system.”

“Data center is not even 10% of the business at this point. I think it could be much greater. I think the business is going to grow anyway. But I think that the data center piece can be — will be our fastest-growing piece of the business, but it’s not to say we won’t build out the chip plant or other things, clean rooms, all kinds of different things that we can do.”

“I mean the company is bigger. And so I do think as you see load growth…it [Quanta] will grow and it will grow at I’ll consider high upper single-digit growth, organic growth. And as you — look, it’s bigger. So every year gets bigger, the CAGR gets bigger. And so it’s hard for me to get my head around. Can we grow faster, we grow — certainly can grow more. And there’s more verticals and more ways to provide solutions. The returns are better from my standpoint because we — our supply chain is a big piece of this as we go forward and how we look at the supply chain level. So look, I think our returns grow faster, kind of the same pace on organic growth. We will have years at 5%, 6% and years at 9% to 10%. I just — that’s what you’re going to see.”

“I mean I still think we can expand margin. I do. I’m not saying I wouldn’t lean into the company and say this is going to be a technology play, and we’re going to expand margins that much. But the returns from my standpoint, as our vertical supply chain gets better, really, the investment is minimal and you take on more scope, and that scope creates more value. We need to get paid a little quicker in areas. I think utilities are vice versa, they’ll hold cash until the end, put it in rate base at the end of the year. So that profile has always been that way, difficult for us to kind of get that piece of the DSOs. But as we take more — if we’re taking more lump sum, if we’re doing more EPC, our vertical supply chains, all of our front-end services require much less capital. So the company has become much less capital concentric to some degree. So I do think the returns will continue to climb faster probably than margin.”

Bloomberg Green has published two articles recently discussing the two primary bottlenecks preventing faster buildout of electrical infrastructure in the U.S., Europe, and around the world. Those two bottlenecks are transformers (some delayed 3 to 5 years) and skilled, craft labor (it takes ten years to train a lineman and about 4 years to train an engineer to do lower-voltage work).

(By the way, I bet the third bottleneck Bloomberg publishes on is either large combine cycle gas turbines or the permitting process).

And it is not lost on me that Quanta has the largest skilled technical workforce in the industry (by far) and that it has vertically integrated (through acquisitions) to now manufacture electrical transformers in the U.S. (which is important given the trade war and increasing geopolitical tensions with China). And having homegrown access to these two bottlenecks provides Quanta with a massive competitive advantage over the competition at a time when electrical demand/load growth is projected to grow at rates not seen in 20 years. At the recent Bernstein Conference Duke said, “the first thing they ask is, do you have your transformers? Yes, we have them. Do you have your — lots of different things. It’s just where is your labor, how you’re getting labor, all those kind of things that we can answer and when you can answer all those with — the hard questions and show up and do it and do it on time, that’s where you get the solution that we talk about daily.”

To conclude, Quanta is one of the leading electrical grid builders in the country. According to Goldman Sachs, it has built 50% of the transmission lines in the U.S. (well over 50% of the high voltage lines), and has 15% overall market share of T&D (transmission and distribution), and it has expanded its total addressable market organically and through acquisitions into building renewable assets (such as solar farms, wind farms, hydrogen pipelines, LNG, etc), building out long-haul fiber, manufacturing transformers in the U.S., and even constructing data centers (with its recent acquisition of Cupertino Electric, one of the premier builders of data centers in the U.S.). Prior to the Cupertino acquisition, nearly all of Quanta’s work was performed outside or underground, but Cupertino brings them inside the facility (expanding into this very fast growth market).

Quanta is also currently a key solutions provider on the largest clean energy infrastructure project in United States history. Quanta has the most skilled, best trained, largest technical craft workforce in the industry because it trains them in-house at the trade-school college it acquired back in 2018. For this reason, it self-performs 85% of its work, which is a competitive advantage in the industry, because it means Quanta has the capacity to even take on the job, but also because it gives Quanta a better chance of getting the work done on budget and on time. Quanta is a leading builder of critical infrastructure in the U.S. across multiple verticals, and therefore I think a key to the reindustrialization of America and positioned to benefit from decades of trillions of dollars in infrastructure spending.

One last point on the high P/E. Quanta was able to grow EPS at roughly 20% rates over the last decade with no electrical load growth. And its business growth is supported (buoyed) by the regulated spend requirements of utilities. And now, for the first time in really twenty years electricity demand is expected to grow at 2.5% to 3% for the next several years driven by the electrification of everything, re-industrialization (on shoring of critical manufacturing and supply chains), hardening of the electrical grid from extreme weather events, transitioning (over time) to a renewables-based economy, and the continued digitization of the economy (including massive AI demand).

Disclosure: John Rotonti is an investor in and the portfolio manager of the Bastion Industrials and Infrastructure Portfolio, which owns shares of Quanta.

Disclaimer: This article is intended for informational purposes only and does not constitute tax, financial, or legal advice. Investing carries risks, including potential loss of principal. Consult a qualified professional for personalized recommendations and to ensure compliance with applicable tax laws and regulations.