Trane Q4:2024 Earnings

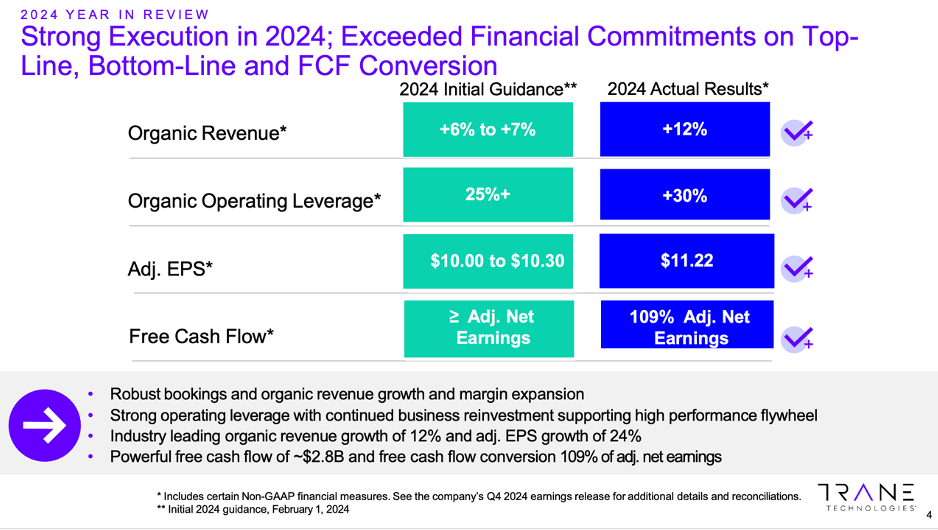

Trane Technologies’ (NYSE: TT) full-year 2024 organic revenue increased 12%, adjusted operating margins expanded 130 basis points, and adjusted EPS grew 24%. This was Trane’s fourth consecutive year of adjusted EPS growth of at least 20%. Trane’s 2024 free cash flow (FCF) grew 30% to $2.789 billion, which equates to a FCF margin of 14% and FCF conversion (FCF-to-adjusted net income) of 109%. It generated a 2024 return on equity (ROE) of 35% (up from 31% in 2023) and a return on invested capital (ROIC) of 18% (up from 15% in 2023).

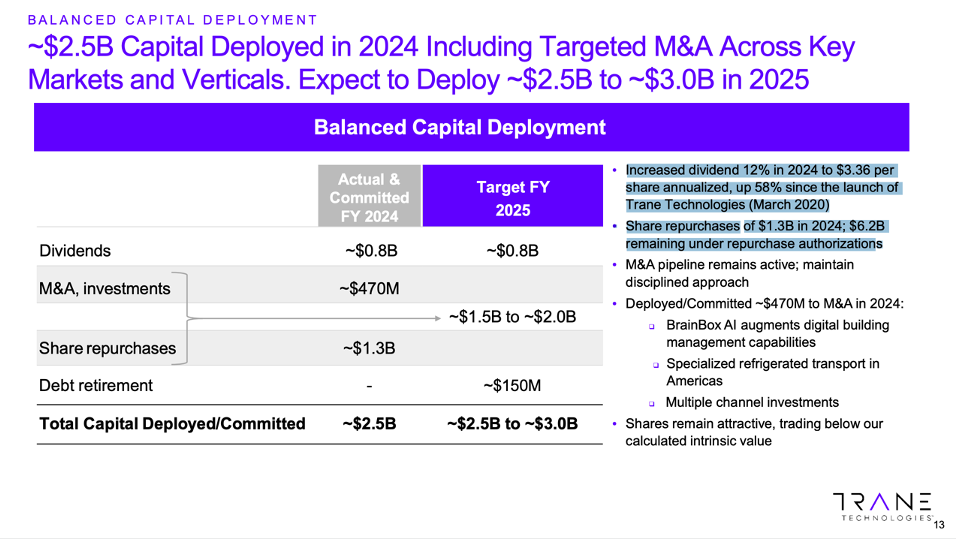

In 2024 Trane increased the dividend 12% and allocated $2.5 billion of total capital ($470 million to M&A, $760 million to dividends, and $1.3 billion to share repurchases). For reference, in 2023 Trane deployed $2.4 billion ($900 million to M&A, $684 million to the divi, and $750 million to share buybacks). Trane is committed to consistently reinvesting into the business (see quotes below) and to returning 100% of FCF to investors over time through a growing dividend and share repurchases.

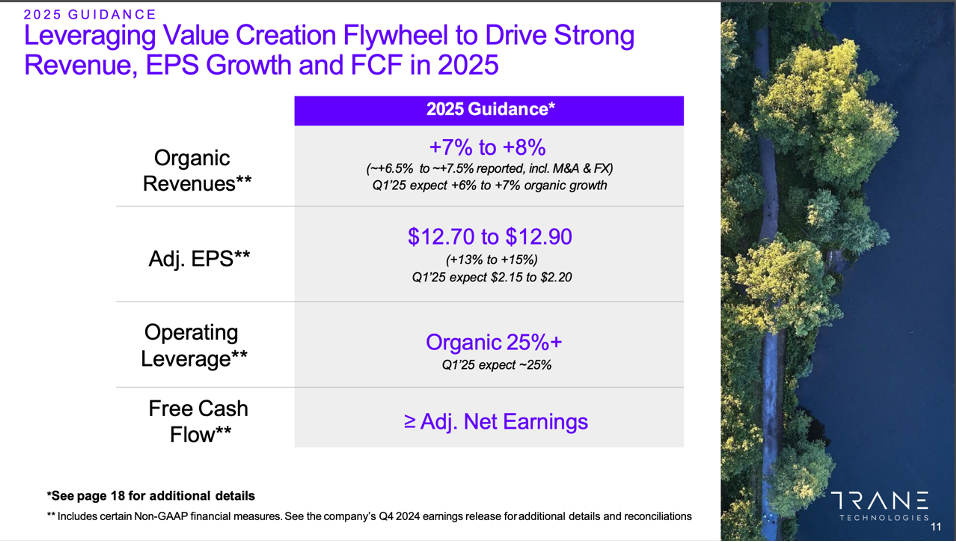

For 2025 management has guided for revenue growth of 6.5% to 7.5% (organic revenue growth of 7% to 8%) and for adjusted EPS to grow 13% to 15% to $12.70 to $12.90.

Trane is one of the highest quality industrial technology companies in the world and it’s getting better, and it’s positioned to profitably grow from the long-duration secular growth tailwinds of decarbonization, energy efficiency, and re-shoring/onshoring. Its commercial HVAC segment (CHVAC) sells highly complicated and customized (applied) HVAC units into mega projects such as data centers, semiconductor foundries, medical facilities, universities, and skyscrapers. Yes, its data center business has been growing like a weed, but data centers are only one of 14 commercial verticals that it sells into. So, its business is diversified by vertical and geography. Additionally, and most importantly to the investment thesis, it has a large and growing installed base (in 42,000 buildings) and these applied units are so complicated and customized that they provide a roughly 30-year lifetime of higher-margin service revenue that is equal to 8 – 10x the initial cost of the machine. This service revenue is higher-margin, predictable, and almost all of it is still in front of the company (has not been recognized yet). I believe the services business will provide Trane with durable growth and transform the company into an even higher-margin, higher-ROIC business over the next 10-20 years. In other words, I think we are still in the early stages of a long-duration profit cycle at Trane that should drive a long runway of 10%-15% per-share growth.

Key Quotes from the Q4:2024 Earnings Call:

“Our backlog is very, very elevated, which gives us a lot of visibility into 2025, and that’s why Chris and I could speak with so much confidence about the guide that we’re putting forward. It gives us great visibility. And the other thing that we track a lot of is the pipelines and these are orders before they become orders, that activity remains very, very robust. As far as data centers go, look, data centers have been a strong vertical for us for decades and they’ll be a strong vertical for us well into the future. As far as the news about new competitor coming out of China and the impact that will have, we’ll see, I can’t comment on that. I could just comment on what we’re seeing right now. And we’re seeing a lot of growth in data centers and we’re seeing a lot of pipeline activity in data centers. I had the opportunity to listen to the earnings call from Meta last night. And if you listen to them, they would say that they’re building out their infrastructure and that’s part of a competitive advantage that they have. So it doesn’t appear as though they’re going to be slowing anything down. But we’ll wait and see, but everyone needs to understand that we are much more than just data centers. Data centers are strong. They’ve been strong in the past. We’re really good in that vertical. But we’re really good in 13 other verticals that we track very, very closely.”

“We expect to deliver top-quartile financial performance over the long term, consistently and reliably for our shareholders. This is core to our culture and central to how we set our targets and execute our strategy across our global portfolio. 2024 was a standout year for the company. I’m proud of how our global teams exceeded our targets, top to bottom. We closely track top quartile performance against our core peer group and believe our performance will rank in the top quartile on organic revenue growth, up 12% as well as adjusted EPS growth up 24%. We also delivered free cash flow of $2.8 billion or 109% free cash flow conversion, enabling us to make key strategic M&A investments while raising our dividend and returning significant cash to shareholders through share repurchases.”

“Relentless investment in innovation, growth, people, culture and our business operating system have yielded clear benefits over time, demonstrated by our strong track record. Since 2020, we’ve delivered a revenue compound annual growth rate of 12%, expanded our adjusted EBITDA margins by 400 basis points and delivered free cash flow conversion of 108%, while deploying approximately $12 billion of capital.

We believe that consistent business reinvestment is key to our long-term success. For over a decade, we’ve added a high level of incremental investments each year in high-ROI projects.”

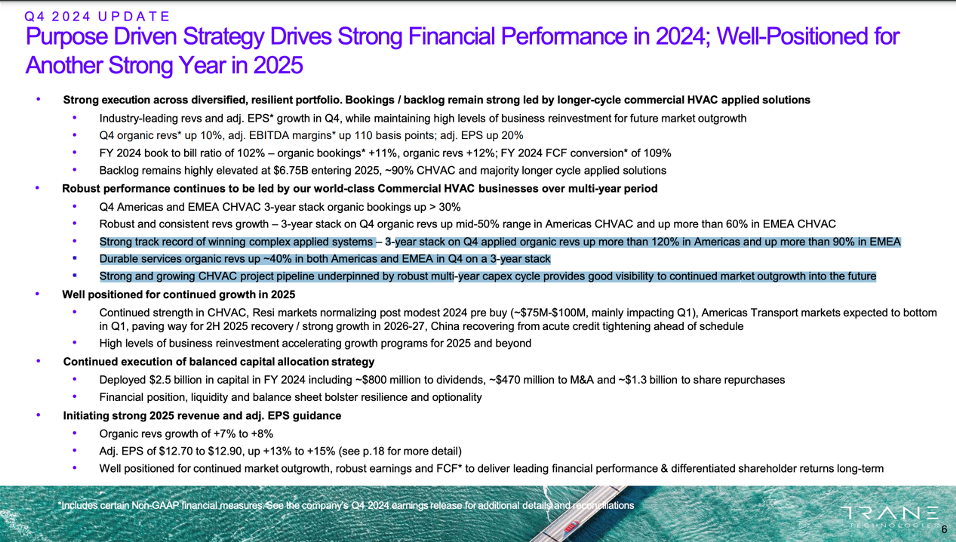

“Organic bookings for full year 2024 were strong, up 11% with a book-to-bill ratio of 102% on top of 12% organic revenue growth. This contributed to a highly elevated backlog of $6.75 billion entering 2025.”

“Our teams are excelling in complex bespoke applied projects, which are key to the multi-year CapEx cycle, especially in high-growth verticals. For instance, three-year stack organic revenue growth in applied systems for our Americas and EMEA Commercial HVAC businesses is up over 120% and 90%, respectively. Applied systems offer a durable service tail of eight times to 10 times the initial equipment cost over their lifespan, meaning our strong growth in applied solutions presents tremendous service opportunities with higher margins that are largely still ahead of us.”

“Just understand 8 to 10 over the life of the asset, right? So the asset is going to add 30 years and the asset cost $1 million, think of it at $8 million in service over that time period. But yes, I mean there is the maintenance that happens. And then obviously, at some point in the useful life, you tend to do our renewals for it where you’ll change out controls or make it run more efficiently just because technology continues to advance. So we’re very comfortable with that number. We’ve done a lot of analysis on that with the installed base. So I’m very comfortable with the 8 to 10 times over the life of the asset.”

“I would add – think about our applied solutions, which impact many of those 14 verticals. Revenues in applied are up over 120% in the Americas, Commercial HVAC business over the last three years. In the EMEA business, it’s up more than 90%. And that is building an installed base that then drive services that think of that as a few years after the installed base, the service revenues start to apply post-warranty period. That’s largely in front of us. So it’s a very durable tail.”

“Chris makes me use a seven-year CAGR on that. So that’s where the high single digits comes from and it’s very high, high single digits. But look, we were up mid-teens or low-teens, I’m sorry, in the fourth quarter low-teens for the full year. Our service business now from a dollar basis is $6.5 billion. And just tremendous growth that we’re seeing there. And if you think about our backlog, right, which is predominantly on commercial HVAC, predominantly applied, that’s really where our service business was designed around our applied solutions. And the more complex those solutions become, the more propensity for the OEM to do the service work. So – but we’ll keep our guide at the high-single-digits, but think about $6.5 billion that’s growing at a close to 10% rate per year in the last couple of years have been in that double-digit range. As you said, it’s a very resilient business.”

“We like the margins in the service business. It’s higher margins when you think about what we’re delivering to customers and making sure that their products are running efficiently. As Dave has described in the past, the service business is rapidly evolving from running to go fix something that’s not working effectively to now making sure that the equipment is always optimized, right. It may be running, you may think it’s up, it’s operating well, but the fact is it may be operating inefficiently and therefore, that’s a really nice opportunity for us. So it gives us a lot of confidence that we should be driving organic leverage 25%, or better. And a reminder, services is a third of the enterprise revenues. It remains a third of the enterprise revenues.”

“Our order grade for Commercial HVAC in the Americas was up high single digits. On a two-year stack, it’s over 20%. On a three-year stack, it’s over 30%. So we continue to see tremendous growth in our Commercial HVAC business. As far as the verticals, yes, we track 14 different verticals and we’re seeing growth, yes, we’re seeing growth in data centers. It’s been a strong vertical for us in the past. It’s going to be a strong vertical for us in the future. But we’re seeing broad-based growth. And if you think about it, I mean, the revenue for the Americas for the year was up over 20% and we had growth in 13 of the 14 verticals. The only vertical that did not show growth was Life Science and it’s been challenged all year, but we’re very optimistic about the future there. So think about that. We’re showing broad-based growth and you would expect that from Trane Technologies with the broad-based portfolio of products and services that we have. We didn’t design our portfolio of products to serve a particular vertical. We designed it to serve the market, and that’s exactly what we’re doing. And if you take that with our direct sales force with deep domain expertise knowledge at both a technical level and then within a vertical level, you could understand why we’re being able to have this broad-based growth. So we’re very excited about what we’re seeing in Commercial HVAC.”

“Our customers know that our solutions are green for green, good for the planet, and good for the bottom line. Our relentless investment in innovation powers our flywheel of market outperformance and strong free cash flow. With this momentum, our proven business operating system and our uplifting culture, we are well positioned to deliver a leading growth profile and differentiated shareholder value into the future.”

“We believe residential markets have largely normalized and are returning to our long-term framework of GDP plus growth. The Americas transport refrigeration markets are expected to bottom in the first half of 2025, paving the way for a second-half recovery and strong growth in 2026 and 2027. In addition, the challenges associated with our actions in the second half of 2024 to tighten credit policies in China are improving ahead of our initial expectations. Given our consistent performance over time, we are confident in our ability to deliver strong results in 2025.”

“This slide provides a snapshot of our fourth-quarter performance, showcasing strong execution across the board. Organic revenues were up 10%, adjusted EBITDA margin increased by 110 basis points and adjusted EPS rose by 20%. At the enterprise level, we achieved robust organic revenue growth in both equipment and services, up high single-digits and low-teens respectively. Our high-performance flywheel continues to yield results with relentless investments in innovation driving top-line growth, margin expansion, and EPS growth. Please turn to Slide 9. At the enterprise level, we achieved robust volume growth, positive price realization, and productivity gains that offset inflation and high levels of business reinvestment. In the Americas, we delivered 9 points of volume growth and 2 points of price.”

“In the Americas, we anticipate continued strong execution and broad-based strength in core markets with particular momentum in high-growth verticals. Our world-class direct sales force and leading innovation are powerful competitive advantages that enable us to optimize opportunities and drive market outperformance. We expect residential markets to return to a GDP-plus framework in 2025, following a modest pre-buy of around $75 million to $100 million in Q3 and Q4 of 2024. Most of this pre-buy is expected to impact the first quarter of 2025. For the full year, we see mid-single-digit growth in the residential business with a tailwind from the low GWP mix. Turning to transport, we expect relative flat markets in 2025, plus or minus low single digits. The market should bottom in Q1, down about 25% year-over-year, then rebound in the second half aligning with freight market recovery forecasts. While the exact timing and speed are uncertain, ACT predicts a sharp recovery in both 2026 and 2027, up mid-teens each year. We’ve continued to invest heavily during the market downturn and we are well-positioned to outperform as the market comes back.”

“Our 2025 guidance reflects the market dynamics outlined on the prior slide and our optimism about our ability to outperform. It also incorporates our value creation flywheel, emphasizing continued investment in innovation, market outgrowth, healthy leverage, and strong free cash flow. We are initiating 2025 guidance with 7% to 8% organic revenue growth and adjusted earnings per share of $12.70 to $12.90, representing approximately 13% to 15% EPS growth. This includes about 100 basis points of negative FX and roughly 50 basis points of growth from M&A impacting revenue, which together are expected to negatively impact earnings by about $0.20 for the year. We are targeting organic [operating] leverage of 25% or higher, consistent with our long-term goals. We anticipate another year of 100% or greater free cash flow conversion in 2025.”

“So $6.75 billion of backlog at the end of 2024. Again, the majority of that, call it, 90% is going to be driven by Commercial HVAC globally. And then of that, it’s going to be majority applied systems. That backlog, the majority of it will revenue in 2025. So that’s actually fairly consistent with how we’ve seen the backlog in terms of the growth over the last few years that the majority will turn in 2025. There’ll be a small amount that will push out into 2026 and that’s really at the customer demand. But the majority of that backlog will turn within 12 months.”

“We’re driving all of those businesses for 25% or better [operating] leverage into 2025…We have a lot of confidence that we’re going to be able to grow the margins and really the leverage with the investments we’re making.”

“For the fourth quarter, price was a little bit above 2 points. It really has been coming down over the last couple of years and now at a – for the full year in 2024, it was a little bit above 2 points as well. And the Americas would be really the driver there, a little bit above 2 points in the Americas. And Julian, for 2025, we’d expect pricing to contribute about a point to maybe 1.5 points on the full-year revenue growth outlook. So on 7% to 8%, we get 5.5% to 6% or 6.5% around volume and then 1 to 1.5 points coming from price…We’re probably in that 1 point to 1.5-point price range for the year.”

“We remain committed to our balanced capital allocation strategy focused on deploying excess cash to maximize shareholder returns. First, we strengthened our core business through relentless reinvestment. Second, we maintain a strong balance sheet to ensure flexibility as markets evolve. Third, we expect to deploy 100% of excess cash over time. Our approach includes strategic M&A to enhance long-term returns and share repurchases when the stock trades below intrinsic value. Please turn to Slide 13. In 2024, we deployed or committed approximately $2.5 billion through our balanced capital allocation strategy with approximately $800 million to dividends, $470 million to M&A, and $1.3 billion to share repurchases. We made several strategic bolt-on acquisitions, enhancing our AI and digital building management capabilities, expanding specialized refrigerated transport, and making multiple channel investments. Our M&A pipeline remains active and we will continue to be disciplined in our approach. In addition, with $6.2 billion remaining under repurchase authorizations, we have strong flexibility as our shares trade below our calculated intrinsic value. For 2025, we expect to deploy between $2.5 billion and $3 billion in capital. Our strong free cash flow, liquidity, balance sheet, and significant share repurchase authorization provide excellent capital allocation optionality moving forward.”

“Do we think there’s opportunities that comps get hard? Look, we still believe there’s tremendous opportunities here for growth in all verticals, right? If you think about the megatrends around decarbonization and energy efficiency, they’re – they continue to intensify. If you think about reshoring activity in the United States, that continues to intensify. If you think about the multi-year CapEx cycle with mega projects, that continues to have momentum. So we’re very bullish on our commercial HVAC business. I would tell you that the portfolio of products and the innovation that we have there, I know I said in my prepared remarks, we are green for green. When you have a solution that’s very sustainable for the planet and has a great payback for the customer, it’s the greatest place to be.”

“I’m super proud of the team in Asia. I know Asia, it’s only 8% of our revenue, 50% of that’s China, 50% is outside the rest of Asia.”

“So if you think about today, we have 42,000 roughly connected buildings. We have well over 2 million connected assets. We’re getting a lot of data at the building level and at the asset level and we’ll call that structured data. What AI does is, it augments that with unstructured data. And when you combine that, that’s really where you’re able to make buildings operate more efficiently. So our service teams will be a big part of that in the future. And I know you’ve probably heard me speak in the past about demand side management. Look, we’ve done hundreds of thousands of energy audits and we know that about 30% of the energy consumed after the meter is being wasted. And our goal is to help decarbonize that built environment and to get everything back to where the way it was designed to operate. And if we can save that 30%, there’s so much opportunity there well into the future.”

“We have 42,000 buildings, right. So there’s 42,000 potential customers that we already have the data on.”

“For decades now, we’ve had a manufacturing strategy of in-region for-region. So you think about – in the Americas, we have a plant in Mexico. We have over 20 plants in the United States. We have plants throughout Europe. We have plants throughout Asia, some in China, some outside of China. So look, we’ve – in the past, we’ve dealt with tariffs. Should they happen, we’ll react. Do I think they could impact our supply chain? For sure, there’s a little bit of flexibility there, but they will have an impact. But I think we’ve been able – part of our operating system is we understand our cost inputs. And if we see something change, we’re going to react and we’re going to act very quickly to make sure that we stay margin-neutral over time.”

“There’s three elements that really come into the guide of around mid-single-digit revenue growth for residential. The first one would be that mix tailwind from the A2L refrigerant change, right? You can think of that as maybe around 4 points high single-digit price on 65% of the portfolio multiplied by, say, three-quarters of the year impact gets you to around 4 points. The view around a GDP-plus framework would be the second element. Think of that as maybe 3 to 4 points of growth from returning to GDP, IRA tailwinds, right, that money is at the state level and it’s really starting to be deployed. That could be a tailwind for 2025. And then items around consumer confidence, tax cuts, those are all things that could be beneficial to the – to a GDP-plus framework for the year. And then the third element would be the pre-buy dynamic, which is probably around 3 percentage points of a headwind. So altogether, you get into that 4% to 5%-ish range on growth, which is our guide for the year around residential. But to be fair, if it turned out that things were softer in the markets and it wasn’t necessarily growth, but it was flattish, and really the impact to our enterprise revenues would be less than a point. It would be 70 basis points or 80 basis points and we really feel comfortable we’ve got that and it’s manageable within our guidance for the year.”

“We’ve been buying up our independence in our Commercial HVAC business for a long time. And these are great businesses. They’ve had great leaders and just it’s opportunistic for us to buy them off. So nothing has changed there with our strategy. There’s not a lot of them left, unfortunately, because they’re great acquisitions and they become accretive very, very quickly, like almost instantaneously. But that’s just more – it’s just more of the same and we just had one this time, it was actually in Belgium over in Europe…think of it as we’ve been 95% plus direct and it’s these last few percentage points of those independent channels that when they’re ready, we’re ready to kind of fully bring them into the Trane business.”

Key Slides from the Q4:2024 Earnings Presentation

(blue highlights done by me; official source):

FOR EDUCATIONAL AND INFORMATIONAL PURPOSES ONLY. The information provided here is for educational and information purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice.