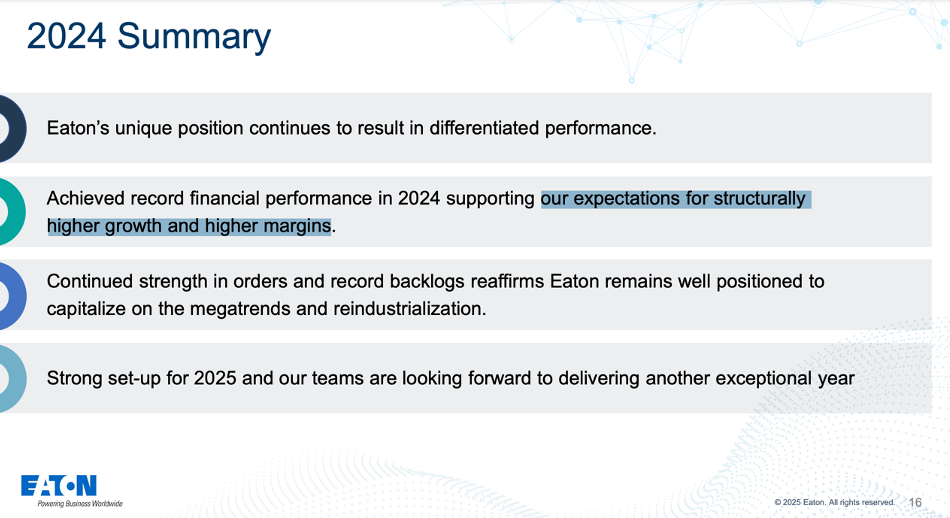

In 2024 Eaton (NYSE: ETN) generated record sales, operating margins, free cash flow (FCF), and EPS. Eaton’s full-year 2024 sales increased 7% (organic sales increased 8%), operating margins expanded 200 basis points, and adjusted EPS grew 18% to $10.80 year-over-year. Eaton’s free cash flow (FCF) grew 23% to $3.5 billion, which equates to a FCF margin of 14% and FCF conversion (FCF/Net Income) of 93%. In 2024 Eaton generated a return on invested capital (ROIC) of 10% (up from 9% in 2023) and a return on equity (ROE) of 20% (up from 18% in 2023). Eaton has increased its ROIC and ROE for four consecutive years.

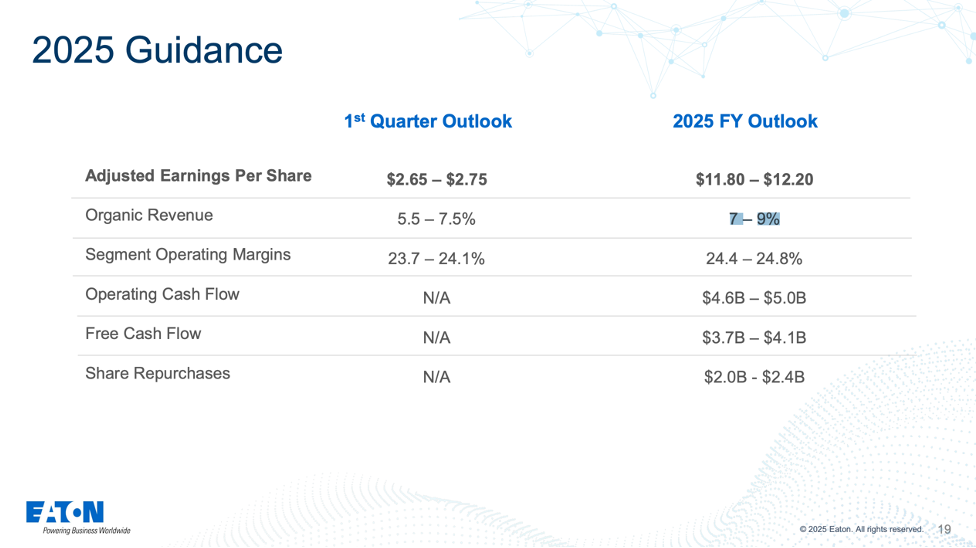

For 2025 Eaton is guiding for organic revenue growth of 7% – 9%, free cash flow of $3.7 to $4.1 billion (growth of nearly 11% at the midpoint), and adjusted EPS of $11.80 to $12.20, implying growth of about 9% to 13% (or 11% at the midpoint). It is also expecting to repurchase $2 billion to $2.4 billion of stock.

Eaton is a multi-industrial technology company (meaning that it is diversified across several important end markets) that I believe is operating with strong business momentum and is very well positioned (almost uniquely positioned) to benefit from multiple long duration secular tailwinds including mega projects and the reindustrialization of America, datacenter buildouts, and the grid buildout and electrification of everything. Because of its exposure to these large and growing markets, as well as its operating leverage on healthy organic growth (30% – 35% incremental EBIT margins) and – in my assessment – highly capable management team that has improved margins through operating efficiencies and capital allocation (divesting lower-margin businesses and acquiring higher-margin, faster-growing businesses), I think Eaton can grow EPS at an annualized rate of 10%-15% over the next five years. And investors also get the growing dividend that yields over 1%.

But Eaton sold off nearly 16% on DeepSeek Monday. (Interesting to note that data centers and distributed IT comprise 17% of Eaton’s business as well). The sell-off was over fears that DeepSeek’s innovations would decrease the amount of capital spent on building AI-specific data centers. I agree that the rate of growth on hyperscaler CapEx allocated to AI-specific datacenters will decline at some point in the future (but that was inevitable, and I believed that prior to the DeepSeek news…these rates of CapEx growth from the hyperscalers can’t go on forever). But I think the overall absolute dollar spend on data centers (both AI and general cloud) will remain massive, and this is especially true if AI is this tectonic technological shift that the tech community believes it is. I believe that even if the combined dollar amount that hyperscalers spend on AI CapEx declines at some point, the amount spent will still remain massive. Either way, it’s important to note that (1) AI is only a subset of data center builds and that (2) data centers are only a subset of infrastructure mega projects. Here are some numbers to highlight that data centers encompass more than just AI and that mega projects encompass more than just data centers…

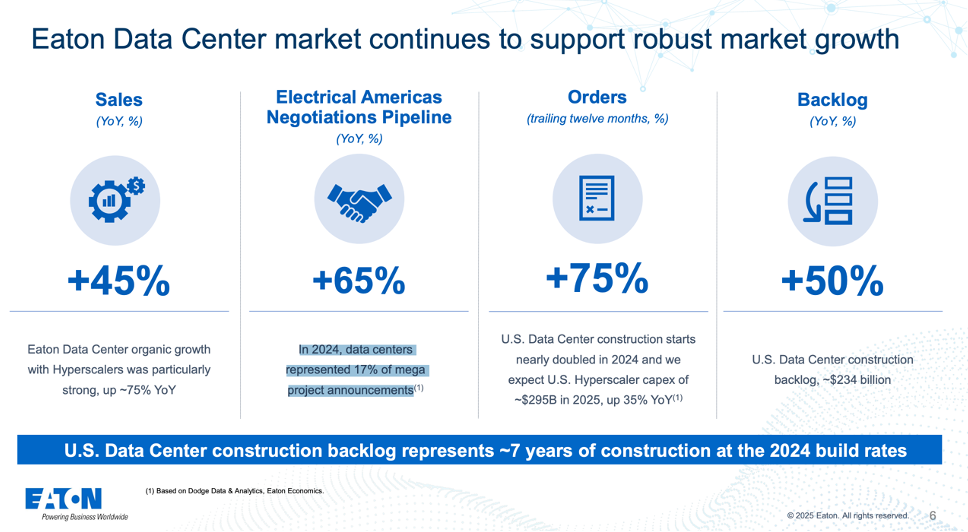

U.S. data center construction backlog is $234 billion. This would take seven years to build at current build rates. These are the numbers Eaton shared in its Q4:2024 earnings call (see below), but to be fair the backlog number is likely even higher now after some recent CapEx guidance (see below).

According to Bernstein, AI is only 15% of Eaton’s data center orders today with the other 85% coming from traditional cloud (Bernstein note January 31, 2025).

Data Centers are only about 17% of Eaton’s total sales.

Through Q4:2024 there have been 569 mega projects announced and the mega project backlog is now $1.9 trillion (up 33% from last year). Only 15% of these projects have started construction. (See below).

In 2024, 17% of announced mega projects were data centers (see below).

“Our current outlook for the replacement of the grid forecasts it will take 40 years to replace ~50% of the current grid, and potentially 80 years to replace 100% of the grid, given the grid on average is 50-70 years old. Despite concerns around AI and data center power demand, we still expect utility spending for T&D, in a medium spending scenario reflecting ~$4.1 trillion of T&D capex needed through 2045.” (Goldman Sachs note January 29, 2025).

Before I end, I’ll leave you with this…despite all the concern that DeepSeek would lead to less data center CapEx, EACH of the four largest hyperscalers (Amazon, Microsoft, Alphabet, and Meta) recently RAISED their CapEx guidance/expectations for 2025. David Kostin at Goldman Sachs recently wrote, “In 2025, the Magnificent 7 companies will boost their capex by 31% year/year to $331 billion. In October, just four months ago, these companies were expected to spend $263 billion on capex (+13%).” So, despite the DeepSeek “scare,” the announced dollar amount of mega-cap CapEx grew in 2025, as did the expected rate of growth.

Key Quotes from the Q4:2024 Earnings Call:

“We summarize our 2024 financial results compared to our original guidance. You may recall that our practice is to set stretch goals for our businesses that are above our external guidance. If we execute well and markets perform as expected, it should put us in a position to exceed our guidance. This occurred again in 2024. Throughout the year, we demonstrated the ability to exceed our commitments and raise guidance on all key metrics. We delivered 8% organic growth, an 18% increase in adjusted EPS, all-time record margins of 24% and a 23% free cash flow, all above our initial guidance. Of particular note, segment margins were up 140 basis points versus the original guidance midpoint and 200 basis points from prior year. And adjusted EPS of $10.80 was 6% above the $10.15 midpoint of our original guide. And as you know, every business deals with a number of market uncertainties, and life has a way of delivering unexpected surprises. So we run the company the way that allows us to absorb these unknown headwinds and still deliver our commitments and hopefully more.”

“The things that we were concerned about prior to Monday [DeepSeek Monday], we’re still concerned about today. And the constraints around whether that’s power availability, whether that’s site availability, whether that’s labor availability or where there will be constraints in supply chain. And as I mentioned, we do believe this market could grow much faster than what we’re anticipating…we’re getting from our customers are much higher than the numbers that we’re baking into our forecast. But we do believe there will be constraints along the way. And those were the things that we were worried about prior to Monday. Those are things that we’re still worried about. I think what happened on Monday with DeepSeek, I think it’s way too early to know how that will influence the evolution of this market. But as I said in my commentary, if history repeats itself, it should mean faster growth, faster adoption, and it could be a good thing.”

“In terms of the agreements [5-year contracts with customers], it’s not exactly take or pay, but there are penalties for order cancellations that are pretty sizable. And I would say, as we look back the last years, we haven’t seen a single cancellation here. So most of the discussions we have, including after the news this week, is about continuing to invest, no distraction on the news this week and continue to build. And you see how our negotiation pipeline development is developing in our backlog as well. So I think the way forward continues to be to accelerate the build-outs.”

“I’d say that we’re once again proud of our team’s execution in the year. We delivered another record year of financial results while reinvesting in the business like never before. But while we’re proud of our progress, we’re not satisfied because we can do so much better. We’re in the right markets, and the identified megatrends are creating some of the biggest opportunities that we’ll see in our lifetime. The growth opportunities are everywhere. Our negotiations pipeline, record orders and strong backlogs are evidence of our ability to convert on the opportunities. And we now have the capacity in place or coming soon to support even faster growth. We have Eaton Business System, we call it EBS, that keeps everyone focused on getting better, running better functions, better factories and better businesses. It’s how we improve our efficiency and expand margins.”

“Overall, we continue to see megatrends noted here as important drivers of secular growth in our markets and why you should expect Eaton to post attractive growth for years to come. And this secular growth is perhaps most evidenced by the megatrend chart that you see on Slide 5 in the presentation. As a reminder, mega project is a project with an announced value of $1 billion or more, and our reference point begins in January of 2021. As you know, we’ve reported this data for a few quarters now, and our conclusion hasn’t changed. Each quarter, we’re seeing an increasing number of projects, higher dollar values and a growing backlog. Q4 was another record with 65 projects announced at a value of more than $150 billion. Through Q4, we’re now at 569 projects with a cumulative value of $1.7 trillion, and the backlog now stands at $1.9 trillion, up 33% from last year. Through Q4, approximately 15% of these projects have started, and we expect a record number of starts in 2025. Many of you have asked the question about cancellation rates, which we continue to monitor as well. To date, cancellations have actually been modest, around 11% and well below historical levels. A couple of pieces of Eaton-specific data. For projects that have started, we’ve won over $1.8 billion orders with a win rate of almost 40%, and we’re in active negotiations on another $3.1 billion of Electrical content. So as you can see from the math, most of these projects haven’t reached a negotiation stage, and we expect our orders to continue to grow.”

“And one of the reasons why we started reporting mega projects a couple of years ago that we saw this fundamental shift in our industry as the world was going through this massive CapEx rebuild cycle, and the size of the projects just have been much larger than what we’ve seen historically. And so we thought it was great to take this data and share it externally, as a way of giving you an indication of what we’re seeing in our business. And the numbers are growing dramatically, as we reflected in the PowerPoint presentation. But to your point specifically around 2024, our business doubled in mega projects in 2024 to over $600 million. Our negotiation pipeline up some 60%, and if you recall, for the overall business, it’s up 41%. So we continue to see an increasing number of projects. And the good news, as we’ve said many times, is that most of the benefit associated with these mega projects is still out in front of us. And as you saw in the data, the number of projects and the size of the projects continue to grow. And it just – we’re really going through a fairly significant CapEx expansion cycle in the U.S. for sure, but around the world.”

“We look at the Dodge data. And in 2024, there were 56 projects that started and around $135 billion in total. And their forecast for this year, for 2025 is actually that we’re going to reach over $300 billion in 114 projects. So even if we don’t – we tend to haircut the starts, we don’t believe in all starts, it’s almost doubled at the rate we saw in 2024. So I think that the message from Craig, I think the key point is the longevity of growth cycle ahead of us.”

“Those are large projects. It takes time between announcement and revenues between three and five years, what we said in the past. And since we started following those projects in 2021, 2022, it’s to be expected that now we start to see the effect. And as Craig said, our sales doubled in 2024 for mega projects versus 2023.”

“As these data center projects have become bigger, some of them are now falling into the category of mega projects. And so clearly, we’re seeing data centers show up in that category as well. I don’t have the exact percentage handy…Yes, I got. We actually said it on the slide. It’s roughly 17%.”

“Given the heightened discussions on data centers this week, I wanted to take a moment to highlight our data center business and why we have so much confidence in our outlook for continued growth. The information on Slide 6 summarizes our sales, negotiations, orders and backlog for our data center business. It includes hyperscale, colos, on-prem data centers and the major categories of cloud, training and inference. And cloud is still, by a wide margin, the largest category. As you can see from the data, the rate of growth is continuing to accelerate with negotiations and orders well ahead of sales. I’ll not read each of the numbers as they speak for themselves, but we’ll ask that you note a few points. Our backlog is rapidly increasing, up 50% over prior year, which was up 70% over 2022. And as you’ve all seen, customers continue to increase their forecast for capital investments. Hyperscale customers alone expect to spend almost $300 billion in CapEx in 2025, up 30% from 2024. And perhaps the most notable number on page is the reference to the seven years. At 2024 build rates, it would take seven years to consume the current backlog. And the data center construction build rate doubled between 2023 and 2024. So any notion that this market will slow down is simply not consistent with any of the data that we’re seeing. The industry will no doubt continue to see innovation and technology developments that reduce costs. And if judged by history, this will be good for the industry and an accelerator of growth. For 2025 and for years to come, we expect data centers to be our strongest market and stand by our previous forecast, which assumed strong double-digit growth.”

“So any notion that this market will slow down is simply not consistent with any of the data that we’re seeing. The industry will no doubt continue to see innovation and technology developments that reduce costs. And if judged by history, this will be good for the industry and an accelerator of growth. For 2025 and for years to come, we expect data centers to be our strongest market and stand by our previous forecast, which assumed strong double-digit growth.”

“I’m not making an industry forecast here because it’s too early. But if you have higher adoption and the data centers are built faster, the inference data centers, most of the bottlenecks that actually create the biggest headache for data center operators will vastly go away. Instead of trying to accommodate gigawatts training centers, if you can accommodate much smaller energy consuming inference centers, the build could accelerate, and that could be a very good thing for us as well. But basically, it will be the same transformers, it would be the same switch gear [in inference data centers as in training data centers]. It will be the same UPS inside the server hall and the software, et cetera. It’s the same portfolio, no disruption there. Having said that, where we are actually working really closely with our hyperscale and multi-tenant data centers is how do we help them building faster, growing their builds and be able to develop this large backlog of seven years in a nice way. That’s the focus. But we got calls with our key customers after Monday [DeepSeek Monday]. The sentiment is still the same. Nothing changed. We keep pushing forward.”

“For the quarter, we generated a Q4 record for adjusted EPS of $2.83, up 11% from prior year. We also delivered record segment margins of 24.7%, up 190 basis points than last year and above the high-end of our guidance. And we continue to see strong market activity. On a rolling 12-month basis, Electrical orders were up 12%, led by Electrical Americas with orders up 16%, and orders were up 10% in Aerospace. This led to another quarter of growing and record backlogs with once again outstanding results in Electrical Americas, up 29% and in Aerospace, up 16% with book-to-bill ratios above one in both businesses. As you can see from the chart, we’re set for another strong year in 2025. Paulo will walk you through our guidance, but we do expect another year of healthy end markets, strong organic growth, margin expansion, improving free cash flow and double-digit increases in adjusted EPS.”

“I will start by providing a summary of our Q4 results, which again includes many new records. We posted fourth quarter record sales of $6.2 billion, up 6% organically or 5%, including 1 point of FX headwind. Hurricane Helene and labor strikes in the Aerospace industry negatively impacted Q4 sales by approximately $80 million or 130 basis points. Operating profit grew 13%, and segment margin expanded 190 basis points to an all-time record 24.7%. Adjusted EPS of $2.83 increased by 11% over the prior year. This is a Q4 quarterly record and near the high-end of our guidance range. This performance resulted in an all-time record cash flow performance, including operating cash flow of $1.6 billion, up 23% on a year-over-year basis and free cash flow of $1.3 billion, up 27% versus prior year. I will now review the segment’s quarterly results followed by a recap of the year.”

“We detail our Americas results. The business continues to execute very well and delivered another record quarter. We set new records for operating profit and margins and posted a Q4 quarterly record sales. Organic sales growth of 9% was driven primarily by strength in data center, along with solid growth in commercial and institutional markets. Without the impacts of the hurricane disruptions to the business, organic growth would have been in the double-digits. Operating margin of 31.6% was up 310 basis points versus prior year, benefiting from higher sales. On a rolling 12-month basis, orders remain at a high level of 16%, demonstrating continued tailwinds from the various megatrends. We had particular strength in the data center market, where activity remains very robust. For example, Dodge data shows U.S. announced data center project starts are up 99% in 2024 and 173% year-over-year in Q4.”

“U.S. data center construction backlog is now estimated to extend out about seven years based on 2024 build rates. Electrical Americas backlog increased 29% year-over-year with a book-to-bill ratio of 1.2 on a rolling 12-month basis. These results closed out a record year for the business, which posted full year revenue of $11.4 billion, organic growth of 13% and margin of 30.2%, up 370 basis points over prior year. With the tailwinds from secular trends, incremental capacity coming online, strong execution and robust backlog, Electrical Americas remains well-positioned as we enter 2025.”

“Before moving to our industrial businesses, I’d like to briefly recap the combined Electrical segments. For Q4, we posted organic growth of 8% and segment margin of 26.7%, which was up 170 basis points over prior year. For the full year, we posted organic growth of 10% and segment margins of 26%, up 220 basis points over 2023. On a rolling 12-month basis, orders were up 12%, and our book-to-bill ratio for our Electrical sector remains very strong at 1.1.”

“Page 10 highlights our Aerospace segment. We posted all-time record sales and Q4 record operating profit. Organic and total growth was 9% for the quarter driven with growth in all end markets with – commercial aftermarket. Without the impacts of the Aerospace industry strikes, organic growth will have been in the double-digits. Operating margin was strong at 22.9%, up 50 basis points year-over-year, mostly from higher sales. On a rolling 12-month basis, orders increased 10% up from 6% in the prior quarter with particular strength in military OEM, commercial OEM and commercial aftermarket. Year-over-year backlog increased 16% and was up 2% sequentially. On a rolling 12-month basis, our book-to-bill for our Aerospace segment remains strong at 1.1. On the full year basis, Aerospace posted 10% organic growth with 23% margins.”

“We show our Electrical and Aerospace backlog updated through Q4. Backlog continues to be very strong with Electrical at $11.8 billion and Aerospace, at $3.7 billion for a total backlog of $15.5 billion. Versus prior year, our backlogs have grown by 27% in Electrical and 16% in Aerospace. They are also increasing sequentially. As noted earlier, book-to-bill ratios for Electrical and Aerospace are 1.1 and 1.1, respectively. The continued growth in our backlog underscores our high-level of confidence in future demand.”

“In addition to our strong backlog growth in 2024, the next page shows the continued strength in our negotiations pipeline supports, our expectation for strong markets and structurally higher organic growth rates. In Electrical Americas, the pipeline has increased nearly four times, since 2019. In fact, the pipeline grew 40% year-over-year, showing acceleration versus our multiyear CAGR of 29%. The year-over-year increase was largely driven by data center, commercial and institutional and utility end markets. Within the commercial institutional end market, growth was driven by education, government and transportation. This is even stronger than the 13% organic growth in our Electrical Americas business, which suggests continued strength going forward.”

“Moving on to our Vehicle segment on Page 11, in the quarter, total revenue was down 10%, including a 7% organic decline primarily driven by weaknesses in the North America, EMEA and APAC light vehicle markets and three points of unfavorable effects. Despite the top line weaknesses, the team executed well from a margin perspective. Operating margin came in at 18.8%, 90 basis points over prior year from improved operating efficiencies. On a full year basis, Vehicle recorded organic revenue down 5% with 18% margins.”

“On Page 12, we show results of our eMobility business. Total revenue was down 11%, including a 10% organic decline, primarily driven by our customers’ program launch and production ramp-up delays and 1% unfavorable FX. Operating profit was $3 million, resulting in operating margin of 1.8% for the quarter. On a full year basis, eMobility posted 4% organic growth with negative 1% margin.”

“Shifting our attention to 2025 on Page 17. We provide our view on end market growth expectations for the next year. As you can see, we continue to anticipate attractive growth markets in nearly all of end markets. We’re expecting double-digit growth in data center and distributed IT, commercial aerospace and electrical vehicles. For data centers, we remain constructive in our future outlook, given the strength and breadth of our secular trends. We continue to see strong demand in data center market with the adoption of cloud computing and acceleration of AI technologies, including inference and training. So as more AI technology emerge, acceleration in AI usage could drive higher consumption of our AI hardware, including our electrical equipment. We also expect solid growth in utility and modest growth across many of our other end markets. So we anticipate weaknesses in commercial vehicle and resi markets. But the change in resi outlook from last quarter is offset with strength in other end markets. And we do not see a change in our overall market growth between 6% and 8%. Overall, 2025 should be another year of significant growth with more than 85% of our end markets seeing growth. Our growth outlook is supported also by a strong order book, a strong record backlog and favorable secular trends. So we remain well positioned to deliver differentiated growth in 2025.”

“Organic growth for 2025 is expected to be between 7% and 9% with particular strength in Electrical Americas at 11.5% at the midpoint. And I’ll also add that healthy end markets combined once again with our large backlog continue to provide premium visibility to support our 2025 outlook. For segment margins, our guidance range is, between 24.4% and 24.8%, is an improvement of 60 basis points at midpoint from our 2024 all-time record margins of 24%. Now on the next page, we have the balance of our guidance for 2025 and Q1. So for 2025, our EPS is expected to be between $11.80 and $12.20, a $12 at the midpoint and up 11% from 2024. And our free cash flow, our guidance is between $3.7 billion to $4.1 billion, up 11% at the midpoint. We also expect to repurchase between $2 billion and $2.4 billion of our shares outstanding. And given our strong cash position at the end of the year and our strong cash generation this year, we will leave plenty of room for strategic M&A.”

“If you look at the EPS [guide for 2025], we are planning today to have the first half to directionally represent 48% of the full EPS guide for the year and the second half as a result, 52%. If you look at the recent past, we used to have a mix between first half and second half of 46% and 54%. So we’re well balanced first half, second half.”

“And the other point I’ll just raise and we mentioned it earlier is that historically, we were living in an inflationary environment. We were getting more price, and we’ve simply anniversaried a number of those price increases from prior years. And quite frankly, our volumes are actually, as we look forward, as Olivier mentioned in his commentary, contributing more to our growth and most of our growth going forward. So a big difference is also the relative amount of price that we’re experiencing in the business because we simply don’t have as much inflation as we’ve had historically.”

“I mean we – coming out of the COVID kind of period when supply chains just got massively disrupted, we were spending weekly calls and daily calls with our suppliers on dealing with supply constraints. And so I’d say for the most part, we’re back to where we were pre-COVID when you think about our internal supply chains. And a lot of those constraints have been, for the most part, resolved…Now, as we think about our longer-term or midterm outlook, we’re certainly constraining our view of the world largely, because we do think the labor continues to be somewhat constrained. If you think about our industries, skilled trades, you’ve seen an industry mix shift. And those industries have been growing labor, at a faster rate than the overall economy. But we still think that is potentially the bottleneck for the industry. And it’s why we’ve, quite frankly, constrained our own view of the rate of growth that we think this market is going to see. It could be better, if some of these labor constraints don’t materialize.”

“So first of all, we are on top of it [tariffs]. We are ready. We know potentially from – depending on what is announced, we know exactly what to trigger. We have – more importantly than that, I think we have a philosophy over time. We moved our production much closer to the consumption side. So that decreases the impact of the tariffs. But we have a playbook. We’ve done that before. We are ready. We know exactly where the – where to apply commercial actions, and we’ll do. We’ll fully compensate with commercial actions if necessary. Hopefully not necessary.”

“So in the first part, I would say what drives growth in utility distribution where we play, there’s a big portion of replacement of aging infrastructure that you probably heard about. The second thing that drives the growth is also the hardening of the resilience part. So think about all the natural events, fires, floods, hurricanes, et cetera, that are getting ready to be more resilient to face those issues. The third piece is about the increased energy consumption. Right. And also, that part of that increase also is a data center story, but there’s more to it. So that’s how the industry plays. If you move that to Eaton and the effects of that in our company, you know that we are heavily weighted to the U.S. distribution network. So we expect this CapEx to be in the high single digits, and it’s consistent with a third-party forecast like S&P or EEI, et cetera. And we think this high single digit, I want to give even more clarity because I think it’s important as you compare Eaton to other electrical players, we see – within this high single-digit market, we see strong double-digit growth in many of the high end of the offers, which is most of what we do. So think about switchgear, regulators, recloser, capacitor. So that part of the market will continue to grow strongly double digits. And there is an offset on the – more on the lower value add of the chain, which is related to single-phase transformers, those poll transformers or line installation equipment, more the hardware piece than some of our competitors are pretty focused on. So it’s a high single-digit growth for us. But there’s a double-digit side that we like the most, and the other part of the market is growing not so fastly. If you go outside North America, if you look at global, I would say China continues to invest very heavily in utility, right, both in generation, in renewables and also in transmission and distribution in China. And electricity, electricity consumption is increasing 7%. It’s very big for a country of that size. So we also expect a strong growth coming from that side of the world as well. In terms of capacity, we talked about capacity. As part of our investments, we are also adding capacity to utility. And we do that in a modular fashion. We do that in a way that can also serve other markets like a transformer could go into data center, it could go into utilities. Some of the switchgear can be used in other end markets.”

“I would say our major areas of interest [for acquisitions] continue to be data centers, utilities and Aerospace, so Electrical and Aerospace. And in terms of the size of the acquisitions, what we’re interested in doing in the short and mid-term is to look at bolt-on acquisitions that can accelerate our organic strategy. So Electrical and Aerospace would be the answer.”

“The large proportion of that [CapEx] is going to be growth. The team is doing a good job actually rationalizing our CapEx investments. We have managed the tail that has been a principle that Craig has implemented for a number of years. So most of the CapEx would be growth. I would say 80%.”

“But what we said is that where we have capacity constraints, we have made investments that are multiyear investments that more than provide for the capacity to cover our growth forecast in those industries. And so where we’re tight in markets like data center and products like transformers, we’ve made sizable commitments to investments that allow us to cover where we are today and a multiyear view of the capacity that we’re going to need. And so the company, as we committed last time, we’re in good shape. We will not be the bottleneck in the industry. We’re making these capacity investments. We talked about $1.5 billion of incremental growth capacity that we’re putting into the businesses. And that will cover our forecast and provide upside if markets tend to be a bit stronger than what we’re forecasting.”

“I’d say that in terms of what happened at the end of the year, which has us incrementally less enthusiastic in resi [residential], as the Fed cut interest rates, everyone expected that to translate to an improvement in the residential market and borrowing costs for consumers. And that, quite frankly, hasn’t happened as we all know. And so I’d say on the margin, resi got a bit weaker during Q4. And I’d say on the MOEM segment [Eaton’s electrical machinery business], more or less a bottoming out, we think. And maybe there are some green shoots in MOEM. But specifically in resi, we’ve become less bullish on the resi recovery, given the fact that interest rates have remained stubbornly high.”

Key Slides from the Q4:2024 Earnings Presentation

(blue highlights done by me):

Full deck shared by Eaton

Disclaimer: This article is for informational purposes only and should not be relied upon as a basis for investment decisions. Investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. All statements made regarding companies, securities or other financial information contained in the article are strictly beliefs and points of view held by Bastion Fiduciary and are not endorsements of any company or security or recommendations to buy or sell any security.